What is blockchain technology? This question leads us into the fascinating world of decentralized systems, key components, and real-world applications that define the essence of blockchain technology.

What is Blockchain Technology?

Blockchain technology is a decentralized system that enables the secure transfer of digital assets without the need for intermediaries. It is essentially a distributed ledger that records transactions across a network of computers.

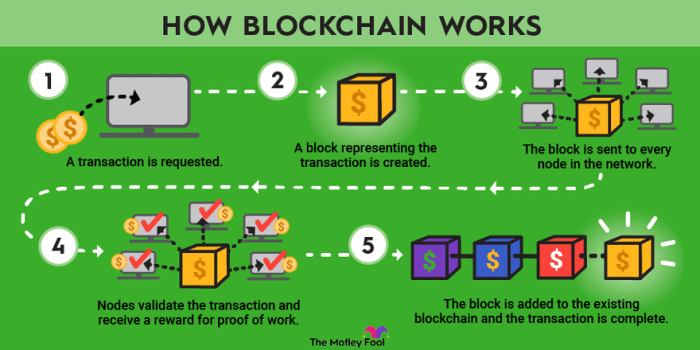

How Blockchain Works in a Decentralized System

Blockchain operates on a peer-to-peer network where transactions are verified by network participants through a process called consensus. Once a transaction is approved, it is added to a block and linked to the previous block, forming a chain of blocks – hence the name blockchain.

- Transparency: Every participant in the network has access to the same information, promoting transparency and accountability.

- Immutability: Once a block is added to the blockchain, it cannot be altered or deleted, ensuring the integrity of the data.

- Security: The decentralized nature of blockchain makes it resistant to fraud and hacking attempts.

Key Components of Blockchain Technology

Blockchain technology consists of three key components: blocks, nodes, and miners.

- Blocks: These are containers that store transaction data. Each block is linked to the previous one, forming a chain.

- Nodes: These are individual computers or devices connected to the blockchain network. Nodes maintain a copy of the entire blockchain and validate transactions.

- Miners: Miners are responsible for verifying transactions and adding them to the blockchain. They compete to solve complex mathematical puzzles to validate transactions and are rewarded with cryptocurrency.

Examples of Industries Using Blockchain Technology

Blockchain technology has found applications in various industries, including:

Finance: Blockchain is revolutionizing the financial sector by enabling faster and more secure cross-border transactions.

Supply Chain Management: Companies are using blockchain to track and authenticate products throughout the supply chain, improving transparency and reducing fraud.

Healthcare: Blockchain is being used to securely store and share patient data, ensuring privacy and interoperability between healthcare providers.

Key Features of Blockchain Technology

Blockchain technology offers several key features that make it unique and valuable in various industries. These features include:

Immutability

Immutability is a fundamental feature of blockchain technology that ensures once data is recorded on the blockchain, it cannot be altered or deleted. Each block in the blockchain contains a unique cryptographic hash that is linked to the previous block, creating a chain of blocks that are interconnected. This makes the data stored on the blockchain tamper-proof and secure.

Consensus Mechanisms

Consensus mechanisms play a crucial role in blockchain technology by ensuring that all participants in the network agree on the validity of transactions. Different blockchain networks use various consensus algorithms such as Proof of Work (PoW), Proof of Stake (PoS), and Delegated Proof of Stake (DPoS) to achieve consensus. These mechanisms help maintain the integrity and security of the blockchain network.

Public vs. Private Blockchains, What is blockchain technology

Public blockchains are decentralized networks where anyone can participate, view, or validate transactions. They are open and permissionless, offering transparency and security through consensus mechanisms. On the other hand, private blockchains are permissioned networks where access is restricted to authorized participants. They offer more control over the network and are often used by organizations for specific use cases.

Overall, the key features of blockchain technology, including immutability, consensus mechanisms, and the distinction between public and private blockchains, contribute to its growing adoption and application across various industries.

Benefits of Blockchain Technology: What Is Blockchain Technology

Blockchain technology offers numerous advantages that can revolutionize various industries. One of the key benefits of blockchain is its ability to enhance security and transparency in data transactions. By creating an immutable and decentralized ledger, blockchain ensures that data cannot be altered or tampered with, providing a high level of security.

Enhanced Security and Transparency

Blockchain technology uses cryptographic algorithms to secure transactions, making it extremely difficult for hackers to manipulate data. Each block in the chain is linked to the previous one, creating a transparent and traceable record of all transactions. This transparency helps to build trust among users and eliminates the need for intermediaries in transactions.

- Blockchain enhances security by encrypting data and storing it across multiple nodes, reducing the risk of a single point of failure.

- The decentralized nature of blockchain ensures that no single entity has control over the entire network, making it resistant to cyber attacks.

- Blockchain’s transparency allows users to track the history of transactions, providing a clear audit trail for accountability.

Reducing Fraud and Errors

Blockchain technology has the potential to significantly reduce fraud and errors in various industries. The immutability of blockchain ensures that once a transaction is recorded, it cannot be altered or deleted, reducing the risk of fraudulent activities.

- Smart contracts, which are self-executing contracts with the terms of the agreement directly written into code, automate processes and eliminate the need for intermediaries, reducing the possibility of human error.

- Blockchain’s consensus mechanisms ensure that all participants in the network agree on the validity of transactions, reducing the risk of fraudulent or erroneous transactions.

Cost Savings through Blockchain Implementation

Implementing blockchain technology can lead to significant cost savings for businesses by streamlining processes, reducing transaction fees, and eliminating the need for intermediaries.

- Blockchain automates manual processes, reducing the time and resources required to complete transactions.

- By removing intermediaries from transactions, blockchain reduces costs associated with third-party fees and commissions.

- Blockchain’s transparency and traceability help to streamline supply chain processes, reducing costs associated with tracking and verifying product authenticity.

Challenges and Limitations of Blockchain Technology

Blockchain technology, while revolutionary in many ways, also faces several challenges and limitations that need to be addressed for wider adoption and scalability. One of the main challenges is the issue of scalability within blockchain networks, which can significantly impact transaction speeds and costs.

Scalability Issues in Blockchain Networks

- Blockchain networks, especially public ones like Bitcoin and Ethereum, struggle with scalability due to the consensus mechanisms and the need for all nodes to validate transactions.

- As the number of transactions increases, the network can become congested, leading to slower transaction times and higher fees.

- This scalability issue has been a major roadblock for blockchain technology to be used for mainstream applications that require high transaction throughput.

Environmental Impact of Blockchain Mining

- Blockchain mining, especially in proof-of-work consensus mechanisms like Bitcoin, requires significant computational power and energy consumption.

- The environmental impact of mining, particularly in terms of carbon emissions and electricity consumption, has raised concerns about the sustainability of blockchain technology.

- As the popularity of blockchain grows, the environmental impact of mining activities has become a critical issue that needs to be addressed.

Potential Solutions to Address the Limitations of Blockchain Technology

- One potential solution to scalability issues is the implementation of layer 2 solutions like Lightning Network for Bitcoin or sharding for Ethereum, which can help increase transaction throughput without compromising security.

- Another approach to reduce the environmental impact of blockchain mining is the shift towards more energy-efficient consensus mechanisms like proof-of-stake, which require significantly less energy compared to proof-of-work.

- Furthermore, research is ongoing to develop new consensus algorithms and technological advancements that can improve the scalability, security, and sustainability of blockchain technology in the long run.

In conclusion, blockchain technology offers a transformative solution with its unique features and potential benefits, paving the way for a more secure and transparent digital future.

When starting out in the world of cryptocurrency trading, it’s crucial to use the best crypto indicators for beginners to make informed decisions. These indicators can help you analyze market trends and make profitable trades.

For those looking to enhance the security of their digital assets, using multi-signature crypto wallets is a smart choice. These wallets require multiple signatures to authorize transactions, adding an extra layer of protection.

Mastering top cryptocurrency market analysis techniques is essential for successful trading. By understanding market trends and analyzing data effectively, you can make informed decisions and maximize your profits.